When accounting teams talk about being buried during tax season, the conversation often defaults to volume. Volume is real, but it is not the whole story. The deeper problem is that busy season compresses time around every weak workflow habit the firm has tolerated the rest of the year. If document requests are unclear, if intake moves through too many channels, if review-ready means different things to different people, and if open items depend on memory instead of visible ownership, peak season multiplies the cost of all of it.

That is why tax-season cleanup should be framed as workflow cleanup, not just stamina management. The strongest available source-backed lessons point in that direction. The IRS explicitly advises taxpayers to gather all tax-related paperwork and wait until all tax documents are received before filing.[1] AICPA quality-management guidance emphasizes documented policies, responsibilities, monitoring, and remediation.[3] APQC’s process framing emphasizes standardization and consistency.[4] IFAC guidance commonly supports pairing technology with process redesign rather than treating tools as a substitute for operating discipline.[5] Taken together, those sources support a conservative but practical conclusion: a cleaner season comes from cleaner workflow states.

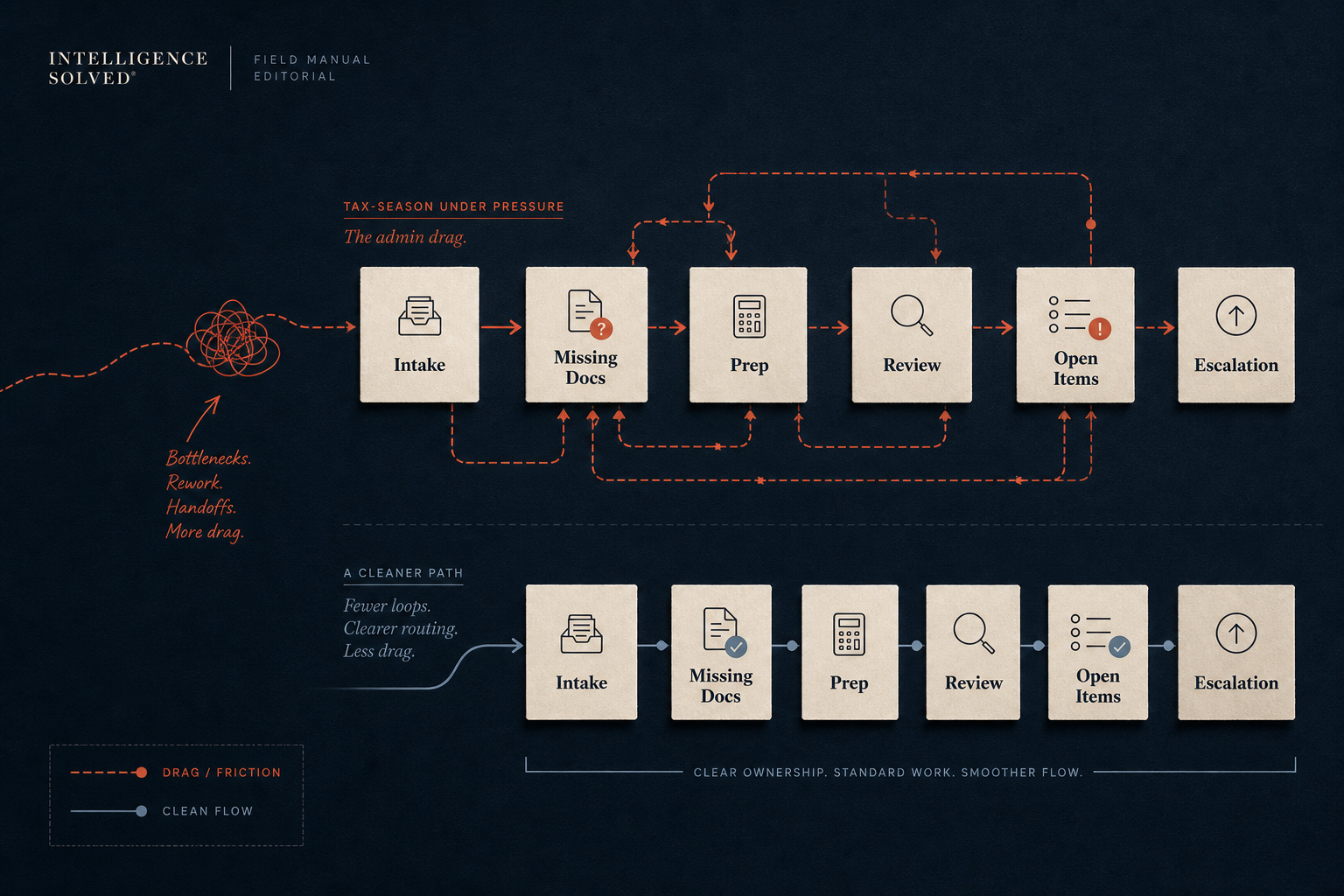

Tax season does not create chaos. It reveals it.

Every firm feels pressure during filing season. Pressure alone is not unusual. What matters is whether the workflow continues to behave predictably when deadlines compress. A healthy workflow can still be busy. A weak workflow becomes noisy. Information arrives out of order, requests get resent because nobody can tell what has already been received, review queues start filling with files that are not truly ready, and secure document handling becomes harder to enforce because the team is trying to keep work moving.

That pattern is why tax-season cleanup should begin with diagnosis instead of blame. If the season feels disorganized, the firm should ask which workflow states are least reliable under pressure. Is the intake state unclear? Is review handoff too loose? Are open items aging without ownership? Are staff working around the system rather than inside it? Those are operating questions, and they are much more useful than broad complaints about busyness.

Busy season is when a firm learns whether its workflow rules are real or merely aspirational.

1. Intake discipline matters more in tax season because the downstream cost of missing documents rises fast.

The IRS guidance telling taxpayers to gather all tax-related paperwork and wait until all tax documents are in hand before filing may sound basic, but it reflects a workflow principle that accounting firms should take seriously.[1] Incomplete intake is not just inconvenient. It forces the rest of the workflow to operate on unstable inputs. A preparer starts anyway, a manager assumes the gap will be closed later, review begins on partial context, and everyone ends up paying for the same missing item more than once.

During slower periods, teams can sometimes compensate for weak intake through experience and extra follow-up. During tax season, that compensation becomes expensive. The number of files is higher, the turnaround expectations are tighter, and every avoidable clarification consumes time that the reviewer or preparer will not get back. That is why intake should be treated as a formal control layer rather than as a prelude to the “real” tax work.

One of the most common tax-season mistakes is allowing the workflow to begin before the file has a trustworthy status. A file may be labeled as started even though several required documents are still missing or ambiguous. That creates a false sense of progress. The work has movement, but not stability. Once enough files accumulate in that state, the firm starts carrying a hidden backlog of future clarifications.

What better intake control looks like in peak season

- a defined required-document list for each recurring return or engagement type

- clear status labels for received, incomplete, unclear, waiting on client, and ready for prep

- a disciplined rule for when the workflow can move forward and when it must wait

- a short escalation ladder for aging missing items

- approved intake channels that can be monitored consistently

These are not glamorous changes, but they are exactly the sort of standardization that process-management guidance supports.[4] The operational value is that they reduce rework later in the cycle, when rework is hardest to absorb.

2. Secure document flow becomes a workflow issue, not just an IT issue.

During busy season, teams are often tempted to accept documents however they arrive, simply to avoid delay. That is understandable, but it creates two overlapping problems. First, the workflow state becomes harder to track because files, screenshots, and clarifications get scattered across multiple channels. Second, secure handling becomes less controlled at exactly the time the firm is under the most communication pressure.

The IRS Dirty Dozen materials are relevant here because they describe scams that threaten taxpayers, businesses, and tax professionals during filing season.[2] While those warnings are not a workflow manual, they support the conservative operational position that tax-season communication and document collection need controlled channels and disciplined handling. In practice, that means the same workflow question matters to both operations and security: where is the authoritative intake path?

If the answer is “wherever the client sends it,” the firm is usually paying a coordination tax. Staff have to search email, confirm whether an upload duplicates something already received, and decide whether the latest file is final or partial. That is workflow drag in addition to security exposure. A cleaner intake lane reduces both.

Operator signs that document flow is too fragmented

- staff are unsure which version of a document is current

- the team cannot quickly tell whether support came through an approved channel

- different people are re-requesting the same item because no single source of truth exists

- review starts before anyone has confidence that the document set is stable

Once the firm notices those symptoms, the right fix is rarely “remind everyone to be more careful.” It is to tighten the intake lane and reduce the number of states the team has to remember manually.

3. Admin drag usually compounds at handoff points.

Tax-season workflows are full of stage boundaries: intake to prep, prep to review, reviewer back to preparer, preparer back to client, and reviewer to final signoff. Those handoffs are where admin drag often accumulates, because every ambiguity that survived the prior stage becomes someone else’s cleanup burden.

AICPA quality-management guidance is helpful here because it emphasizes documented responsibilities and monitoring.[3] In operator terms, that means a file should not change hands without a shared expectation about what was completed, what remains unresolved, and what evidence should accompany the handoff. If the receiving person must reconstruct that context from scratch, then the workflow is relying on human memory where it should rely on visible structure.

This is why some firms feel perpetually stuck in review even when the prep team is working hard. The bottleneck is not merely review capacity. It is that review keeps inheriting files with preventable ambiguity. Every preventable ambiguity expands reviewer labor: re-reading the thread, checking whether support exists, clarifying what the preparer already noticed, and deciding whether to send the file back or resolve it personally.

What makes a tax-season handoff stronger

- a short unresolved-items summary attached to the file

- a visible list of what was received late or remains missing

- a stated review-ready standard that prep can actually use

- a distinction between routine missing support and true judgment-heavy exceptions

Those controls reduce more than time loss. They reduce interpersonal friction. Review feedback becomes cleaner because the file state is clearer, and prep gains a more reliable standard for what “ready” actually means.

4. Review queues become dangerous when they contain too many false starts.

Queue pressure is a normal feature of busy season. The danger comes when the queue is filled not only with genuine work awaiting review, but with files that should not have reached review yet. Operations logic broadly supports the idea that waiting time rises sharply as utilization and queue pressure increase. Even without claiming a tax-specific benchmark, that principle matters because it shows why false starts are expensive under deadline compression. When a reviewer opens a file that is not truly ready, the queue loses capacity twice: once when the reviewer spends time diagnosing the problem, and again when the file returns later for a second pass.

This is one reason firms sometimes feel that everyone is moving but the queue is not shrinking. The queue may be absorbing low-quality entries. Stronger gating does not reduce volume, but it can improve queue quality, which matters just as much during compressed periods.

A practical way to think about this is that review should be protected from avoidable ambiguity. Complex returns and legitimate judgment calls belong there. Basic document incompleteness, preventable intake confusion, and unresolved status questions do not. If they are still showing up in review, the bottleneck is upstream.

5. Checklists matter because busy-season memory is unreliable.

Tax season places heavy demands on recall. Which documents are still missing? Which items were clarified? Which follow-up has already been sent? What was the unusual issue on this file? Under load, even strong staff become less reliable at carrying that context informally. That is why standard work and checklist discipline matter. They reduce dependence on memory at the exact moment memory is least trustworthy.

The support for checklists in accounting is indirect but still useful. AICPA quality-management guidance emphasizes documented procedures and monitoring.[3] APQC emphasizes standardization and consistency.[4] Broader operations and high-consequence work literature also supports the reliability benefits of structured checklists, though that evidence should be treated as analogous rather than tax-specific proof.

The practical takeaway is straightforward: in busy season, the workflow should remember more than the people do. A checklist is not bureaucracy for its own sake. It is a way of making sure recurring controls survive deadline pressure.

Useful tax-season checklist layers

- required-document completeness

- approved-channel confirmation

- unresolved-question summary

- review-ready signoff criteria

- open-item aging and escalation triggers

If those layers are missing, the team will likely compensate manually. That compensation is where admin drag hides.

6. The most expensive repeated task is usually the document chase.

Every accounting team knows the feeling of re-asking for the same information. It is one of the clearest examples of admin drag because it consumes skilled attention without creating accounting value by itself. Industry accounting operations coverage often returns to document chasing and delayed client response as recurring pain points, which supports treating this as a structural issue rather than an isolated client-behavior problem.[6][10]

Repeated chasing happens for more than one reason. Sometimes the client is late. Sometimes the original request was unclear. Sometimes the intake path was fragmented. Sometimes the team cannot tell what was received already. Sometimes the missing item is being requested by the wrong person at the wrong stage. Workflow cleanup does not eliminate the need for follow-up, but it can make follow-up more targeted, more visible, and less repetitive.

That is also where better metrics help. Instead of tracking only whether the return finished, firms can examine internal proof objects such as first-pass document completeness, number of follow-up touches per file, and the age of missing-item requests. Those indicators help leadership see whether delay is being driven by client responsiveness, weak request design, or poor workflow visibility.

A document chase is not just a communication burden. It is a signal that the workflow still cannot see its own input state clearly enough.

7. Technology helps more when the workflow has already been narrowed.

IFAC guidance commonly supports pairing technology with process redesign.[5] That matters because tax-season cleanup is often misframed as a tooling problem. A firm under pressure may try to solve document chaos, review drag, and status ambiguity simultaneously by adding more software or more automation. Sometimes a better tool genuinely helps. But if the workflow itself remains undefined, the tool usually inherits the same confusion.

The safer approach is narrower. Choose one repeated friction layer and make it more controlled. For example: define the intake states for one recurring tax workflow, standardize the missing-item request format, or formalize what must be present before review starts. Once that smaller system is legible, technology has a place to help without crossing into judgment-heavy work it should not own.

This is also where later AI use becomes more realistic. Governance-oriented sources such as NIST AI RMF and professional guidance from AICPA/CIMA and IFAC support human oversight, accountability, and bounded use.[5][8][9] In practical terms, that means AI is far better suited to drafting a follow-up request or summarizing open items than to making final tax judgments. Workflow cleanup is what makes that distinction operationally usable.

8. What a cleaner tax-season workflow actually looks like

A cleaner season is not one where no one feels pressure. It is one where the workflow remains legible even while pressure rises. Leadership can see which files are blocked, why they are blocked, whether the issue is client-driven or internal, and what the next action should be. Staff do not need private memory to reconstruct status. Review is not routinely asked to diagnose basic intake failures. Missing documents age visibly instead of disappearing inside personal notes and inboxes.

That kind of workflow does not require perfection. It requires stable states. The team needs a shared language for received, incomplete, unresolved, ready for prep, ready for review, and waiting on client. It needs visible ownership for open items. It needs a standard way to surface exceptions. Those are simple ideas, but they create the foundation that makes peak-season work less chaotic.

9. Capacity planning improves when blocked work is separated from active work.

One reason tax-season capacity is hard to manage is that many firms keep too much blocked work mixed into the same visible queue as truly active work. A return may appear to be in progress even though the next real step depends on client response, document clarification, or resolution of an open item. When those states are blended together, leadership cannot easily distinguish workload from waiting. The result is distorted capacity planning. Managers see a large in-process inventory but cannot tell how much of it is moving and how much of it is stalled.

That distinction matters because process-management literature commonly treats work-in-process visibility and queue discipline as prerequisites for practical improvement.[4] AICPA quality-management guidance also supports clearer responsibility, monitoring, and remediation.[3] In a tax workflow, the conservative interpretation is that firms should know whether a file is actively being prepared, waiting on client input, waiting on internal review, or paused for exception resolution. Those are not cosmetic labels. They determine whether the next lever is staffing, follow-up, or escalation.

When blocked files remain mixed into active production counts, the firm can easily overestimate how much useful prep work is underway. Staff then get pressed for speed on the wrong cases, reviewers inherit more partial files, and leadership loses the ability to tell whether the bottleneck is labor capacity or input readiness. Separating those states does not solve the season by itself, but it improves operational judgment about where attention is actually needed.

Useful distinctions for tax-season queue visibility

- ready for prep versus waiting on client documentation

- actively prepared versus paused for internal clarification

- review-ready versus sent to review prematurely

- awaiting final approval versus awaiting client authorization or signature

- exception-heavy work versus routine recurring work

Those distinctions help leadership avoid treating every late file as the same problem. Some files need faster production. Others need clearer requests, tighter gating, or faster escalation on missing items.

10. Review quality depends on how well the file explains itself.

During peak season, review becomes less efficient whenever the file does not carry enough context forward. The reviewer should not have to rediscover the intake history, reconstruct what the preparer already checked, or guess whether an unresolved question is material or merely pending. AICPA quality-management guidance supports documented procedures and clear responsibilities.[3] In operator terms, that means a file should arrive at review with enough context to support a controlled decision, not just enough data to reopen investigation.

This is especially important because reviewers are often the most expensive coordination surface in the workflow. If the reviewer must spend significant time rebuilding context, that time is no longer available for true judgment-heavy work. A cleaner file reduces that waste. It explains what was received, what remains open, what assumptions are being avoided, and whether the file is waiting on a routine missing item or a substantive exception.

That does not require long internal memos. In many firms, a short unresolved-items summary and a standard review-ready checklist are enough to improve the quality of review entry. The point is not to add narrative for its own sake. The point is to reduce hidden reconstruction work.

A file that cannot explain its own state will force the reviewer to do workflow cleanup before review can even begin.

11. Standardization is most useful where the work is repetitive, not where judgment is unusual.

One reason workflow standardization gets resistance in tax environments is that teams correctly recognize that not every return is identical. That observation is valid, but it can be misapplied. APQC process-improvement framing and broader finance operating guidance support standardizing repeatable steps while preserving room for exception handling and professional judgment.[4][5] The question is not whether all tax work can be standardized. The better question is which parts of the workflow are repetitive enough to deserve a default operating rule.

In most firms, the repetitive layers are easy to spot. Required-document requests recur. Intake-status labeling recurs. Missing-item follow-up recurs. Review-ready criteria recur. Escalation timing for aging items recurs. Those are exactly the places where standardization reduces unnecessary variation. By contrast, unusual source documents, contradictory information, and materially judgment-heavy tax issues should still move through human review with explicit care.

This distinction matters for tax-season cleanup because teams often delay standardization while waiting for a perfect system that can handle every edge case. That standard is too high. A narrower and safer goal is to standardize the recurring coordination work so that the scarce judgment work is easier to see and easier to protect.

Good candidates for standard work in busy season

- initial document-request templates for recurring engagement types

- approved intake channels and what counts as received

- file-status definitions and ownership rules

- review-ready checklists for routine return categories

- escalation timing for unanswered client requests

Those moves are modest by design. They shrink unnecessary variation without pretending that professional judgment can be reduced to a script.

12. Workflow metrics matter when they help the team intervene earlier.

Tax-season reporting often emphasizes output totals and deadlines met. Those are necessary results, but they are lagging indicators. They tell the firm what happened after the workflow already absorbed the stress. Operationally, it is often more useful to track indicators that reveal pressure earlier: document completeness on first submission, open-item age, number of follow-up touches per file, review return rate, and the share of work entering review without satisfying the stated gate.

The support for this kind of measurement comes indirectly from source material that emphasizes process control, monitoring, and cycle-time discipline.[3][4] The exact dashboard should vary by firm, but the governing idea is simple: measure the workflow states that create rework before they become deadline problems. If leadership waits to react until everything shows up as a late file, the workflow has already hidden the root cause.

Metrics are especially helpful when they change the quality of conversation. Instead of saying, “the team is overloaded,” a partner or manager can ask more useful questions. Are too many files entering prep incomplete? Is one reviewer receiving too many false-start files? Are follow-up touches concentrated in a specific client segment? Is the open-item queue aging because requests are unclear or because the firm is not escalating? Those are operationally answerable questions.

Used carefully, metrics also reduce the temptation to overreact with a broad systems overhaul. A firm may discover that the biggest seasonal gain is not a total process replacement, but a better first-pass intake checklist and clearer blocked-state visibility. That kind of answer is often less dramatic and more valuable.

13. A realistic tax-season improvement plan should start smaller than leadership expects.

Firms under pressure often want a comprehensive tax-season reset. The instinct is understandable, but it can create another form of drag: too much change introduced in the middle of already compressed work. IFAC and other transformation-oriented guidance support pairing technology with process redesign, but they do not require an all-at-once rollout for every recurring workflow.[5] In practice, a smaller controlled cleanup is usually safer.

That might mean choosing one return category, one intake channel, one review queue, or one recurring document-chase pattern and improving that narrow layer first. The point is to make one part of the season measurably more trustworthy. Once the team can see the before-and-after state in that lane, broader change becomes easier to evaluate. Without that control, firms may stack new expectations onto the same unstable workflow and call the extra strain transformation.

This is also where workflow cleanup becomes more credible than abstract AI messaging. A firm does not need to believe in sweeping automation claims to benefit from a better intake gate, a clearer waiting-on-client state, or a tighter review entry rule. Those are immediate operating improvements. They also create the conditions for future automation to be safer, narrower, and more accountable.

Questions worth asking in a tax-season workflow review

- Can we tell, without digging through threads, what is still missing on a file?

- How many files in review are not truly review-ready?

- Which open items are older than expected, and why?

- Where are we re-asking for information because the intake state was unclear?

- Which coordination tasks could be simplified once the workflow states are cleaner?

- Can we separate active work from blocked work without relying on staff memory?

- Does every reviewer receive a consistent handoff summary, or does context have to be rebuilt manually?

- Which recurring steps are repetitive enough to standardize now, even if unusual files still need custom handling?

If the answers are difficult to produce, that is already useful evidence. It means the season is being managed with more memory and improvisation than the firm can safely afford under load.

The bottom line

Tax-season workflow cleanup is not about making people work harder. It is about reducing the amount of avoidable coordination work that the season is amplifying. IRS guidance supports complete document gathering and waiting for all relevant documents before filing.[1] IRS scam warnings support tighter communication and document-handling control.[2] AICPA quality-management guidance supports documented procedures, responsibilities, and monitoring.[3] APQC and IFAC support standardization and process redesign as operating levers.[4][5] The conservative interpretation of all of that is clear: firms reduce admin drag by making the workflow easier to trust.

That means tighter intake states, cleaner approved channels, stronger handoffs, more visible open items, and more disciplined review gates. Once those states are stable, technology and automation can actually support the season instead of adding another layer of ambiguity. Until then, the real work is not hype. It is operational housekeeping at the exact places where the season keeps breaking the workflow open.

If you want to reduce admin drag without inventing a bigger systems project

Intelligence Solved helps accounting teams clean up one workflow at a time: clarify the states, define the handoff, protect the review boundary, and add automation only after the process is trustworthy.

Sources

- IRS, “Get ready to file in 2025: IRS highlights what taxpayers should know before filing in 2025,” irs.gov.

- IRS, Dirty Dozen tax scams overview, irs.gov/newsroom/dirty-dozen.

- AICPA/CIMA, quality management standards resources, aicpa-cima.com.

- APQC, process and finance benchmarking resources, apqc.org.

- IFAC Knowledge Gateway, digital transformation and practice guidance, ifac.org/knowledge-gateway.

- Accounting Today, accounting operations and workflow coverage, accountingtoday.com.

- IRS paid preparer due diligence resources, irs.gov.

- NIST, AI Risk Management Framework, nist.gov.

- AICPA/CIMA general professional guidance resources, aicpa-cima.com.

- Thomson Reuters Institute, tax and accounting operations coverage, thomsonreuters.com.