The reason this topic matters is simple: bookkeeping work is cumulative. When one month starts with weak intake and fuzzy ownership, the problems do not stay contained. They flow into reconciliation, review, close timing, partner confidence, and eventually client trust. That is why the most useful question is not “How do we get more output from the team?” It is “Where does work stop moving cleanly, and what evidence tells us that is happening?”

Authoritative finance and accounting sources do not usually write in the same language as a bookkeeping operator trying to survive month-end. They talk about cycle time, process standardization, workflow management, exception handling, documentation, and internal control. But those ideas map directly to the day-to-day experience inside a bookkeeping firm. A document chase is an upstream input problem. A review bounce is a handoff failure. A list of stale open items is an exception-aging problem. A reviewer who has to re-read the thread before touching the file is absorbing the cost of missing workflow visibility.[1][2][3][4][5]

The hidden cost is not just delay. It is the conversion of judgment into coordination labor.

Bookkeeping and CAS teams are not paid primarily for moving information from one inbox to another. The real value is judgment, interpretation, review discipline, and reliable financial organization. Yet many teams lose their best hours to low-grade coordination work: re-requesting statements, clarifying what is missing, reconstructing file status, and determining whether an exception belongs with prep, reviewer, owner, or client. Those tasks may feel small in isolation, but at the workflow level they create a predictable drag on cycle time and reviewer capacity.[1][2][3]

That interpretation is consistent with the broader finance operations literature. APQC’s benchmarking framework treats process standardization and cycle-time management as core performance levers, while Deloitte’s finance transformation materials repeatedly point to manual gathering, fragmented systems, and spreadsheet-heavy processes as barriers to a faster and more controlled close.[1][2] BlackLine’s close-management materials emphasize reconciliations, unmatched items, and exception handling as central workstreams precisely because unresolved exceptions hold work open longer than the team expects.[3]

Seen this way, workflow drag is not a soft complaint about busyness. It is a resource-allocation problem. Skilled accounting attention is being redirected away from review, judgment, and cleanup quality toward remembering status, re-asking for support, and translating unclear handoffs. That is why firms can feel fully occupied and still struggle to create a smoother close: the labor is real, but too much of it is being burned on coordination overhead.

This distinction is important for leadership because coordination overhead can look like dedication. The team is active. Messages are being sent. Files are moving. Questions are being answered. But activity alone is not proof that the workflow is healthy. In a weak workflow, the business can mistake compensating effort for actual control.

When operators say “the file moved, but it still was not ready for review,” they are describing a workflow design failure, not just a staffing complaint.

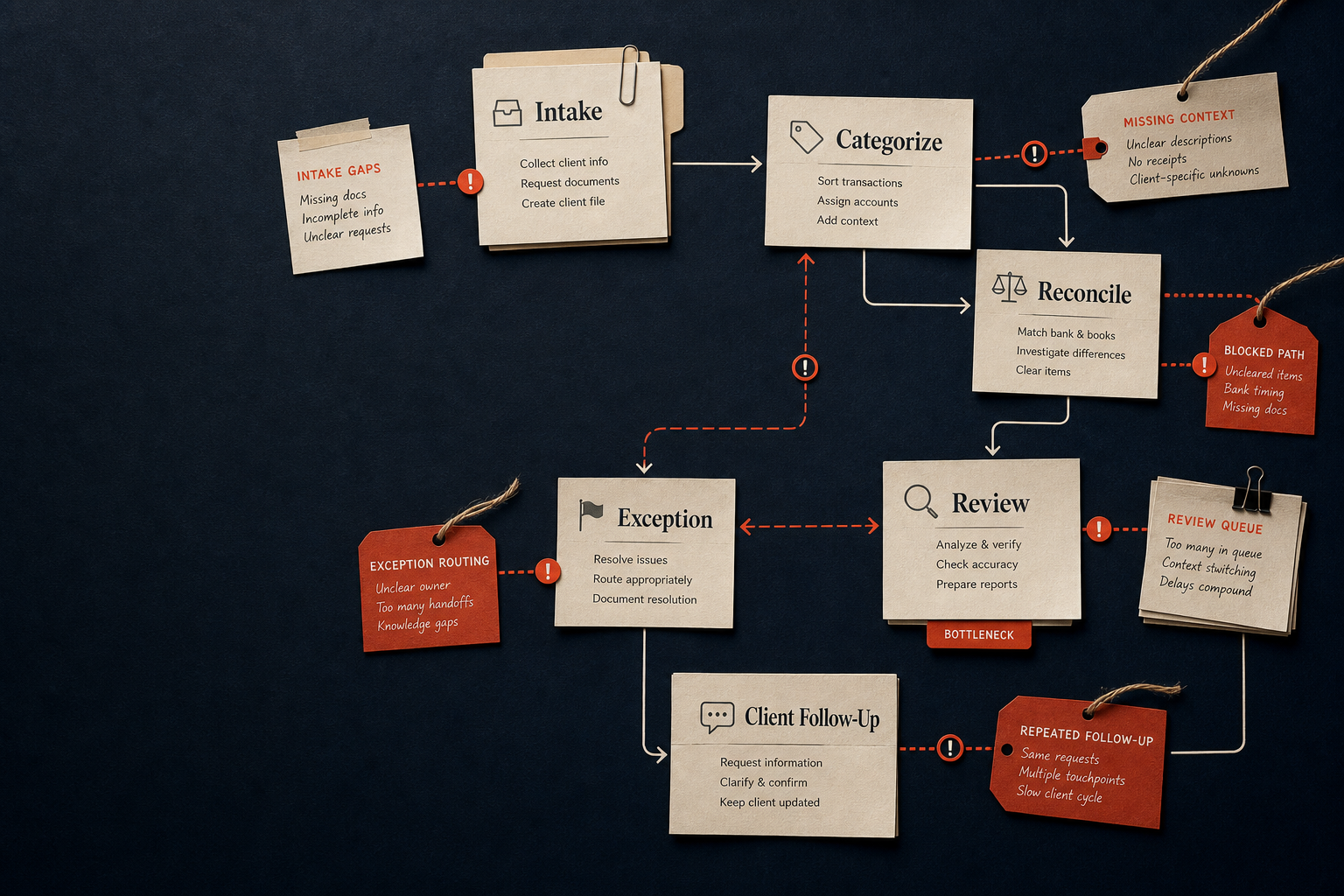

1. Intake failure is usually the first invisible bottleneck.

The first failure is often not a wrong entry or a missed reconciliation. It is the moment a team begins work on incomplete support. Even taxpayer-facing IRS guidance is useful here because it reflects a basic operating truth: filing should not start before the relevant documents are assembled. The IRS explicitly tells filers to gather all tax-related paperwork and wait until they have received all their tax documents before filing.[6] A bookkeeping firm can apply the same logic to recurring monthly work. Starting early on incomplete support may feel proactive, but if the intake process does not distinguish between complete, partial, unusable, and missing items, the team is building downstream work on unstable inputs.

This is where document chaos becomes workflow chaos. A statement in the wrong inbox, a merchant report missing one settlement period, or a client response that answers the wrong question can all force later rework. Industry accounting operations coverage routinely describes document chasing and delayed client responses as recurring friction points for bookkeeping and CAS teams, which is why intake cannot be treated as pure administration.[5][12] Intake is an operating control. It determines whether prep can begin confidently, whether review will inherit ambiguity, and whether follow-up can be escalated based on visible rules instead of memory.

In many firms, intake problems stay hidden because the team compensates around them. Staff search old emails, re-open prior-month request lists, or quietly continue prep while telling themselves the missing item will arrive later. That adaptation can make the workflow look resilient when it is actually fragile. The cost only becomes obvious when review starts and everyone discovers that the file never had a stable input state in the first place.

That is why intake should be treated as a quality gate, not merely as a communication step. A controlled intake process answers three questions before serious work begins: what was required, what was actually received, and what remains ambiguous. If those questions are unclear, the workflow is already borrowing time from prep and review.

What better intake control looks like

- A clear required-items list for each recurring workflow, not a vague request for “anything else you have.”

- Visible receipt states such as received, received-but-incomplete, unusable, waiting on clarification, and ready for prep.

- An approved channel policy for intake, especially during tax and close periods when secure document handling matters.[6][7]

- A missing-item ladder that determines when reminders escalate and who owns the next move.

None of those controls require flashy AI. They require workflow discipline. APQC’s process-management framing is helpful because it emphasizes reducing unnecessary variation and improving consistency.[1] The practical lesson for a bookkeeping firm is that document collection should behave like a system, not a scavenger hunt.

2. Prep-to-review handoff breaks when “done” and “reviewable” mean different things.

One of the most expensive phrases in a bookkeeping firm is: “It’s ready for review.” If reviewer experience consistently shows that “ready” really means “mostly assembled, but still missing context,” then the team has a handoff definition problem. Reviewer time starts getting spent on context reconstruction, missing support checks, and determining whether the preparer already flagged the issue or simply missed it. In workflow terms, the file may have crossed a stage boundary without satisfying the standard required for that stage.

That is why handoff quality matters more than raw activity volume. A high-output prep team can still create reviewer drag if the ready-for-review standard is weak. IFAC guidance on digital transformation and finance operating models supports the broader point that unclear ownership, poor workflow visibility, and weak approvals increase control risk and slow work.[4] AICPA quality-management guidance is also relevant because it emphasizes documented policies, responsibilities, monitoring, and remediation.[8] In operator language: if review standards are not explicit, the reviewer becomes the cleanup system.

Bookkeeping teams usually feel this in several recurring ways:

- Owner or personal-spend questions remain unresolved when the file is handed off.

- Uncleared transactions are listed but not explained well enough for a reviewer to act.

- Loan, draw, or contribution ambiguity is left for a senior reviewer to sort out from scratch.

- Support exists somewhere, but is not attached, labeled, or summarized in a reviewable way.

The fix is not to demand more effort from reviewers. The fix is to create a real review-ready standard with proof objects. That might include an exception summary, unresolved-item count, support checklist, and a simple statement from prep about what still needs judgment. BlackLine’s emphasis on exception handling and reconciliation status helps here because it reinforces that unresolved items are not background noise; they are central workflow objects that should remain visible until they are cleared or escalated.[3]

A useful handoff standard also lowers emotional friction inside the team. When the reviewer trusts the handoff, feedback becomes more specific and less personal. When the handoff is unclear, every reopened file feels like an indictment of prep quality even if the real problem is a missing workflow definition. That matters because recurring reopen loops can quietly erode trust across roles.

Better handoffs therefore do more than save time. They stabilize expectations. Prep knows what evidence must travel with the file. Review knows what is supposed to be resolved before the file arrives. Leadership gains a clearer signal about whether delays are coming from true complexity or from weak operating discipline.

3. Exception handling is not waste. Invisible exception handling is waste.

Exceptions are normal in accounting work. Unusual transactions, incomplete support, mismatched reports, or ambiguous owner activity are precisely the kinds of issues that require real human judgment. Professional guidance from AICPA/CIMA supports the conservative position that unusual, incomplete, or unresolved matters still require human oversight and professional judgment.[9] The goal is not to eliminate exceptions. The goal is to stop them from going dark.

When an exception has no visible owner, no aging signal, and no escalation path, the team starts paying for it repeatedly. One person notices it, another asks about it later, a reviewer rediscovers it, and a client receives another request without a clean status explanation. That repeated handling is the hidden cost. It looks like work moving, but it is actually work circling.

That is why exception queues are one of the most useful proof objects in a bookkeeping workflow. If the team can see the age of unresolved items, the share of files blocked by missing support, and which exceptions are waiting on client response versus internal decision, leadership gets an actual operating picture instead of anecdotes. BlackLine’s educational material around close management consistently treats unmatched items and exception handling as major accounting workstreams.[3] A bookkeeping firm can apply that same logic on a smaller scale.

Useful operator questions about exceptions

- How many files are blocked by unresolved exceptions right now?

- How old are those exceptions?

- Which ones are waiting on client input versus internal judgment?

- How many reviewer bounces are caused by unresolved exceptions that should have been surfaced earlier?

If the team cannot answer those questions quickly, the bottleneck is not just “too many exceptions.” It is weak workflow visibility.

How recurring bookkeeping edge cases turn into workflow debt

One reason bookkeeping teams underestimate workflow drag is that the root causes rarely arrive labeled as “workflow failures.” They arrive as one-off edge cases: support is missing for owner spending, the merchant processor report does not line up to the statement period, a loan balance changed without an obvious memo trail, or the client answered a question in a way that created new ambiguity instead of resolving the old one. Each item looks local. Over time, the pattern becomes systemic.

This matters because the finance-operations literature does not treat exceptions as random noise. It treats them as workflow objects that require visible control, aging awareness, and ownership if the close is going to stay predictable.[2][3] When a bookkeeping firm lacks that structure, the same class of exception can be reopened by prep, rediscovered by review, escalated to a manager, and eventually bounced back to the client with no shared summary of what has already been checked. That is not an accounting-quality problem alone. It is a memory problem inside the operating system of the team.

The practical consequence is that firms start paying senior staff to rebuild context repeatedly. A senior reviewer is not only deciding what the accounting treatment should be. They are first reconstructing how the issue got here, what support has already been requested, what explanation was already attempted, and whether the issue should have been escalated earlier. The more often that context has to be rebuilt from scratch, the less real review capacity the firm actually has.

What good exception control usually includes

- a short written definition of what counts as a true exception versus routine prep work

- a visible owner for each unresolved issue

- an aging view so old unresolved items cannot disappear into the file

- a basic escalation path for issues waiting on client input, internal judgment, or outside-party records

- a review note format that summarizes what is known, what is missing, and what decision is needed

None of that requires claiming a specific benchmark or pretending every firm should run the same software stack. It simply follows the control logic emphasized by close-management and quality-management sources: unresolved work needs to remain legible until someone actually resolves it.[3][8]

4. Repeated follow-up loops are a real workflow cost, even when nobody reports them as one.

Many firms track whether the close finished, whether the reconciliations were completed, or whether the return was filed. Fewer firms track the coordination cost required to get there. That is a problem because repeated nudges, inbox searches, reminder drafting, and “just checking status” messages consume the same finite staff capacity that could otherwise be used for review and cleanup. Industry workflow commentary in accounting repeatedly returns to client document chasing and delayed responses as practical pain points, which supports treating follow-up as part of the workflow, not an external annoyance.[5][12]

In practice, repeated follow-up loops usually signal one of four underlying issues:

- The original request was not standardized enough.

- The workflow does not clearly show what has been received and what remains missing.

- The exception belongs to the wrong person or wrong stage.

- The client is being asked for information through channels that are hard to track or secure.

The IRS Dirty Dozen warnings are relevant here in a narrow but important way. They reinforce that tax-season communications and document exchanges are not just speed problems; they are also secure-handling problems.[7] That supports a controlled-channel intake policy and reduces the temptation to let workflow state fragment across email threads, texts, and ad hoc uploads.

Once follow-up is treated as a measurable operating burden, the team can track better indicators: document-chase touches, percentage of files complete on first submission, age of missing-item requests, and percentage of intake arriving through approved channels. Those are operational signals, not vanity metrics.

5. Cycle time only improves when the team attacks the right layer.

Leadership teams often feel the pain of delayed close or review backlog and respond by pushing harder on labor. More reminders. More check-ins. More late effort. But if the root problem sits upstream in intake, handoff quality, or exception visibility, more labor simply helps the team process the same confusion faster. APQC’s cycle-time orientation is useful because it keeps attention on the system, not just on effort.[1]

Days-to-close, review queue age, and exception aging are all valid workflow indicators because they show whether work is moving predictably or accumulating hidden friction.[1][2][3] But those metrics should be interpreted carefully. A shorter close is not automatically a better operation if the shortcut came from weaker review discipline. The better standard is a controlled close: one where the team can explain why work is delayed, where exceptions sit, what remains unresolved, and who owns the next action.

The right operating goal is not “make the team move faster.” It is “make the workflow easier to trust.”

What a trustworthy close looks like in practice

A trustworthy close is not just one that finishes. It is one that can be explained. Leadership should be able to answer a short list of operating questions without chasing three people for status: which files are blocked, why they are blocked, whether the block is internal or client-driven, what exceptions are aging, and what review work is waiting on unresolved support. When those answers are easy to get, the team gains something more important than speed: shared situational awareness.

Deloitte’s finance transformation framing is helpful here because it repeatedly ties performance to more controlled processes rather than to heroic effort alone.[2] BlackLine’s close-management language also reinforces the importance of visible tasking and exception tracking.[3] A bookkeeping firm does not need an enterprise command center to apply that lesson. It needs a workflow state that can be inspected quickly and trusted by the people doing the work.

This is also why “we are busy” is often a weak diagnosis. A team may be busy because volume is high. It may also be busy because the workflow keeps recreating the same coordination work. The difference matters. If the underlying issue is weak status visibility, bad handoffs, or recurring exception rediscovery, adding more effort can hide the structural problem for a month without actually solving it.

Signals that the close is controlled instead of merely completed

- reviewers can tell which files are truly review-ready without opening every thread

- open items have visible owners and aging

- missing support is logged before it turns into a surprise at review

- leadership can distinguish client delay from internal rework

- staff do not need private memory to know the next move

Those conditions make later automation easier because the workflow already has stable states. Without stable states, AI tends to inherit the same ambiguity the team was already carrying.

6. This is where AI actually becomes useful.

AI is most useful after the workflow rules are clear enough that repetitive coordination can be separated from judgment. Professional guidance from IFAC, AICPA/CIMA, and NIST consistently emphasizes governance, oversight, accountability, and human review for AI-enabled processes.[9][10][11] That means the good early use cases are not “let the model decide accounting treatment.” They are narrower tasks around the repetitive coordination layer.

That distinction matters because bookkeeping firms often evaluate AI at the wrong altitude. They ask whether a model can do bookkeeping, when the more practical question is whether the workflow contains repeatable coordination tasks that are stable enough to support assistance. If the intake states are clear, the follow-up ladder is defined, the review-ready standard exists, and exceptions remain visible, then AI can be applied to narrow jobs inside that system. If those conditions are not true, the model is being asked to compensate for missing workflow design.

NIST’s AI Risk Management Framework is especially helpful because it centers governance, risk awareness, and trustworthy deployment rather than hype.[10] In practical terms, that supports a conservative implementation path: choose a bounded workflow, identify where the model is assisting, document where human review remains mandatory, and make sure accountability does not disappear just because a tool drafted the output. AICPA/CIMA and IFAC guidance point in the same direction by reinforcing oversight and human accountability for AI-enabled accounting processes.[4][9]

Examples of safer early use cases, framed conservatively, include:

- drafting follow-up requests based on a defined missing-item list

- summarizing open exceptions before reviewer handoff

- routing items according to a pre-defined workflow rule

- maintaining status visibility around what has been received, what is still missing, and what is blocked

What AI should not do is silently cross the judgment boundary. If the underlying issue involves unclear support, unusual transactions, or classification ambiguity, the literature supports keeping human review and accountability in place.[9][10][11] In other words: automate the coordination burden around the work before trying to automate the judgment inside the work.

Why workflow state matters more than model capability

A strong model inside a weak workflow often produces a weaker business outcome than a modest model inside a well-controlled workflow. The reason is simple. In bookkeeping operations, the real risk is often not that the first draft will be imperfect. The risk is that nobody will know what to trust, what to verify, what stage the work is in, or who owns the next move. Governance sources focus on exactly those concerns: trustworthy deployment depends on controls, visibility, and accountability, not just on raw tool performance.[9][10][11]

That is why a useful AI install usually starts with a narrow question such as: can the workflow automatically prepare a first follow-up draft once a required document is marked missing? Can it summarize the unresolved items that must be reviewed by a senior accountant? Can it keep a visible record of what has already been requested so the next person does not start from zero? Those are workflow questions. They are much more operationally defensible than broad “AI transformation” claims.

7. The first practical fix is rarely “install more software.”

Firms under pressure often assume the answer is another portal, another dashboard, another automation layer, or another tool promising a cleaner month-end. Sometimes a better tool does matter. But the literature across process improvement, quality management, and finance transformation is much more consistent on a different point: technology works better when paired with process redesign, role clarity, and visible control points.[1][2][4][8]

For a bookkeeping operator, that means the first serious fix is usually one of these:

- Define intake states and ownership clearly.

- Create a non-negotiable review-ready standard.

- Make exceptions visible by age, owner, and dependency.

- Separate follow-up drafting and coordination from true accounting judgment.

- Track a short set of workflow metrics instead of only output metrics.

Those changes create the conditions under which software and AI can actually help. Without them, the tools usually inherit the same ambiguity the humans were already carrying.

Another way to say it: the firm does not need to solve every workflow problem before introducing technology. It does need enough structure that technology is operating inside a known lane. When intake states are undefined, exceptions are invisible, and review boundaries are implied rather than written down, the tool becomes another participant in the confusion. When those states are visible, the same tool can reduce repetitive handling without diluting accountability.

What operators can standardize immediately without overengineering the firm

One reason workflow cleanup gets delayed is that leadership imagines a huge systems project. In reality, a surprising amount of drag can be reduced with a small set of disciplined standards. APQC’s emphasis on standardization is useful precisely because it does not require the firm to redesign everything at once.[1] Standardization means choosing a few recurring moves that stop the workflow from being reinvented every month.

For example, a firm can standardize how required documents are requested, how missing support is labeled, how unresolved items are summarized at handoff, and what counts as review-ready. None of those actions require a full transformation program. They require agreement. Once that agreement exists, it becomes easier to see where a software tool, portal rule, or AI assist might remove repetitive coordination labor without eroding review quality.

High-leverage standards for bookkeeping teams

- a single intake request format for recurring monthly work

- a short list of approved channels for client document exchange

- a standard exception-summary block attached to handoffs

- a visible definition of “ready for review”

- a lightweight escalation ladder for aging missing items

These are not glamorous changes, but they are often the difference between a workflow that can support automation and one that cannot. They also make leadership reporting better, because the team starts describing work in stable categories instead of one-off stories.

What to diagnose first if your team feels permanently behind

If the firm is feeling month-end pressure, do not begin by asking where the team is lazy or where the software is weak. Start with the place where work most often stops moving cleanly.

- If files start with incomplete support: diagnose intake states, request clarity, and approved channels.

- If review takes too long: diagnose whether ready-for-review actually means reviewable.

- If work keeps reopening: diagnose exception visibility, reviewer bounce causes, and unresolved-item ownership.

- If the team spends too much time chasing: diagnose the follow-up ladder and whether missing items are visible in one place.

That first workflow fix is usually worth more than a broad AI initiative because it reduces the amount of expensive human attention being spent on coordination work the firm should already control.

A practical workflow-audit lens for firm owners and ops leads

If you are leading the firm, the fastest way to understand whether the problem is structural is to stop asking only for completion status and start asking for workflow-state evidence. Can the team show you, in one place, which files are blocked, what class of issue is blocking them, how old the issue is, and who owns the next move? If not, then the business may be managing by memory instead of by workflow.

This is where leadership discipline matters. A workflow audit is not a forensic investigation into every task. It is a simple test of whether the operating system produces legible states. APQC’s standardization logic, AICPA’s emphasis on documented responsibilities, and close-management guidance around exception visibility all support the same practical direction: if the work cannot be summarized cleanly, it probably is not being controlled cleanly.[1][3][8]

Questions worth asking in a live workflow review

- Which files are blocked today, and what exactly are they waiting on?

- How many open items are older than the team expected?

- How often does a reviewer reopen work because support was not actually ready?

- Where does client delay end and internal rework begin?

- Which repetitive coordination tasks could be assisted safely if the workflow states were cleaner?

The answers do not need to be perfect to be useful. They need to be visible enough that the firm can stop confusing activity with control.

The bottom line

Workflow bottlenecks in bookkeeping firms are rarely mysterious. The pattern is familiar: incomplete intake, weak handoffs, unresolved exceptions, and repeated follow-up loops that quietly consume reviewer and manager capacity. The reason these issues matter is not only that they delay work. It is that they divert skilled attention away from judgment and toward coordination labor. Finance operations literature, quality-management guidance, and AI-governance sources all support the same conservative conclusion: better outcomes come from clearer workflow states, stronger review boundaries, visible ownership, and disciplined exception handling—not from pretending more tools will solve a poorly defined process.[1][2][3][4][8][9][10]

If a bookkeeping firm wants automation to help, it should first make the workflow easier to trust. Once the team can see what is missing, what is blocked, what is unresolved, and what still requires judgment, AI has a legitimate place. Until then, the real work is simpler and harder: define the workflow, make the states visible, and stop letting coordination labor impersonate accounting progress.

That conclusion may sound less exciting than a promise of instant AI transformation, but it is more useful. Firms do not need another abstract argument that bookkeeping will change someday. They need a way to reduce the hidden drag that is already stealing time today. The clearest path is usually to tighten one workflow, make one boundary explicit, and create one reliable view of status that the team can trust under pressure.

Once that is in place, every later improvement gets easier. Handoffs improve because the standard is visible. Review improves because unresolved items are surfaced earlier. Leadership improves because workflow states can be inspected instead of guessed. Automation improves because the tool is entering a controlled system instead of replacing one. That is the kind of value that actually compounds inside an accounting operation.

If you want to fix one bottleneck instead of talking about ten

Intelligence Solved helps bookkeeping and accounting teams scope one real workflow, define the human-review boundary, and install the visibility and control layer before automation gets added on top.

Sources

- APQC, process and finance benchmarking resources, apqc.org.

- Deloitte, finance transformation and controllership resources, deloitte.com.

- BlackLine, financial close, reconciliations, and exception-management education, blackline.com.

- IFAC Knowledge Gateway, digital transformation and finance workflow guidance, ifac.org/knowledge-gateway.

- Accounting Today, accounting operations and workflow coverage, accountingtoday.com.

- IRS, “Get ready to file in 2025: IRS highlights what taxpayers should know before filing in 2025,” irs.gov.

- IRS, Dirty Dozen tax scams overview, irs.gov/newsroom/dirty-dozen.

- AICPA/CIMA, quality management standards resources, aicpa-cima.com.

- AICPA/CIMA, general professional guidance resources, aicpa-cima.com.

- NIST, AI Risk Management Framework, nist.gov.

- Thomson Reuters Institute, tax and accounting operations coverage, thomsonreuters.com.

- CPA.com and related accounting technology resources, cpa.com.