Client document chaos is one of the least glamorous problems in bookkeeping operations, which is exactly why it causes so much persistent damage. It hides in repeated reminders, unclear intake states, review delays, and recurring manual work that does not feel strategic enough to name as the core bottleneck. But for many firms, document chaos is the operating condition that sits underneath several other visible frustrations: slow month-end work, frequent reopen loops, overloaded reviewers, and too much staff time spent clarifying whether something was received, where it was received, and whether it was complete.

Accounting operations literature and professional guidance support treating this as a real workflow issue rather than as a personality problem or client-discipline problem. IRS guidance on gathering all tax-related paperwork before filing reinforces the broader process principle that downstream work depends on sufficiently complete inputs.[1] APQC process-improvement framing emphasizes standard work, consistency, and reduction of unnecessary variation.[2] AICPA/CIMA quality-management guidance emphasizes documented procedures, responsibilities, monitoring, and remediation.[3] IRS security-oriented seasonal guidance supports controlled channels and disciplined handling.[4] Industry accounting operations coverage repeatedly returns to document chasing and delayed client responses as recurring friction in bookkeeping and accounting workflows.[5][6]

Put together, those sources support a practical conclusion: document chaos should be treated as an intake-control problem with downstream workflow consequences. The bookkeeping team is not just collecting files. It is managing the quality of evidence entering the rest of the process.

Document chaos is not just clutter. It is unstable workflow input.

When bookkeeping teams complain about missing support, scattered uploads, and repeated follow-up, the surface-level issue sounds administrative. But the deeper issue is that the workflow cannot trust its own starting state. If required records arrive through multiple channels, arrive partially, or arrive without a consistent completeness check, then the bookkeeping process begins on shifting ground. Transactions may be posted provisionally, questions accumulate, and the reviewer inherits a file that looks active but is not truly supported.

That matters because downstream bookkeeping work depends heavily on evidence quality. Even when the task itself is routine, the workflow is only as stable as the records entering it. A repeated mismatch between what the team thinks it has and what the file actually contains creates rework that compounds later: more reminders, more reopening, more private notes, and more pressure on the reviewer to reconstruct what happened. The bookkeeping entry may not be the first failure point. The intake state usually is.

A bookkeeping workflow breaks long before the reviewer says it is broken. It usually breaks when the intake state stops being trustworthy.

The hidden cost is repeated coordination, not just missing files.

It is tempting to define the problem narrowly as “clients are late sending documents.” That can be true, but it is incomplete. The larger cost comes from repeated coordination work created by poor visibility. If the team cannot immediately tell what is missing, what was already received, which version is current, and who owns the next follow-up, then each missing item triggers more than one task. Someone drafts a message, someone checks another channel, someone asks internally whether the item came in elsewhere, and someone later re-asks because the prior state was not visible enough to trust.

Industry workflow coverage commonly identifies document chasing and delayed response loops as recurring operational friction.[5][6] APQC’s emphasis on reduced variation and process consistency supports the view that this friction is not merely a communication annoyance. It is the predictable result of a weak intake design.[2] When the design is weak, the team does not just chase documents; it repeatedly rebuilds context around documents.

This is why document chaos often feels larger than the number of missing files would suggest. The burden is multiplied by every unclear state and every duplicated touch. In practice, a single unclear receipt can become several micro-tasks spread across intake, prep, review, and client communication. Those tasks rarely appear in a strategic dashboard, but they consume a large share of working attention.

Once that pattern is established, the workflow also becomes harder to improve because the team cannot easily see which tasks are real accounting work and which tasks are simply recovering from intake ambiguity. The coordination burden starts to look normal. That is one reason the problem can stay in place for so long.

Controlled intake channels matter because the workflow needs a source of truth.

IRS guidance warning tax professionals and taxpayers about seasonal scams is not a bookkeeping workflow manual, but it does support a conservative operational principle: information exchange during accounting work should move through controlled channels wherever possible.[4] That principle matters for more than security. It also matters for visibility. When the team allows documents to arrive interchangeably through inboxes, text messages, portals, screenshots, and ad hoc uploads, the workflow loses a reliable source of truth.

Once that happens, staff must remember where the latest support lives. Reviewers cannot easily confirm whether a document is current. Duplicate requests become common because the intake state is fragmented. The accounting work may still get done, but the firm is paying for disorder with skilled labor. A controlled intake path reduces that coordination tax because it narrows where the workflow expects to look and what it treats as authoritative.

A practical interpretation of this principle is not that every client will comply perfectly at once. It is that the firm should know which channel is authoritative, which exceptions are tolerated, and how off-channel material is normalized back into the workflow. Without those rules, intake becomes whatever happened most recently rather than what the system can trust.

Signs that the intake source of truth is weak

- staff cannot answer quickly whether a required item was received

- different team members rely on different channels for the same client

- reviewers reopen files because a newer version appeared outside the expected lane

- follow-up messages get resent because no one trusts the current status

- the firm cannot tell how much document delay is client-driven versus internally created

Those symptoms point to a workflow design issue, not just a communication issue.

Clear intake states reduce unnecessary variation.

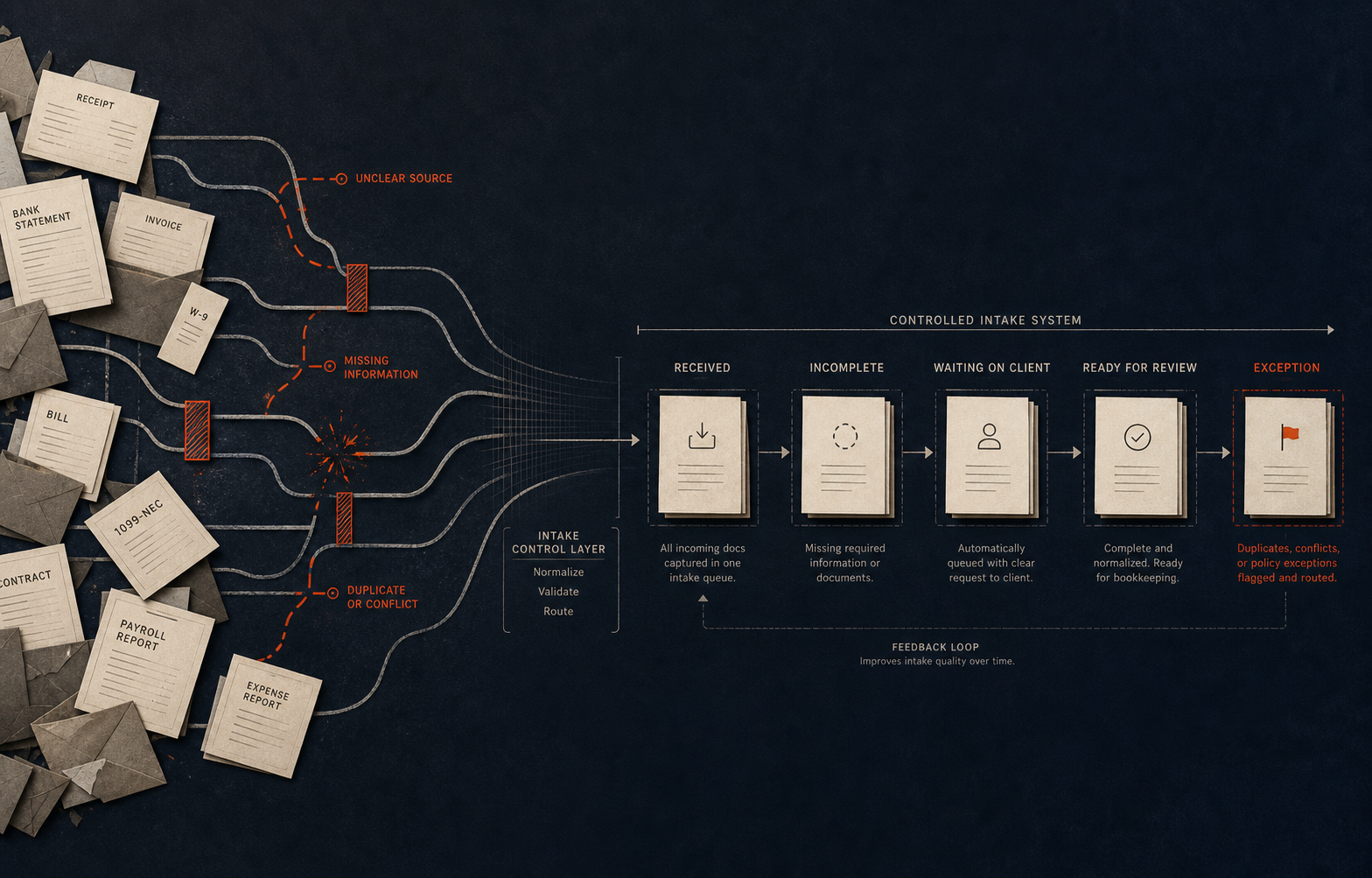

APQC’s process framing supports standardization and reduction of unnecessary variation.[2] In a bookkeeping intake workflow, one of the simplest ways to apply that principle is to define the states more carefully. Many firms function with overly broad labels such as “received,” “in progress,” or “waiting.” Those labels do not carry enough meaning to protect the next step. A file can be marked received even though key records are still missing. It can look in progress even though the real next action is client follow-up. It can appear ready for review even though support is incomplete or contradictory.

Better state design does not require a complex system. It requires more precise categories. For example, a firm may separate received, incomplete, waiting on client, internally unresolved, ready for bookkeeping, ready for review, and exception escalation. The exact labels can vary. What matters is that each state answers a meaningful workflow question. Can the team work now? Does the blocker belong to the client or to internal clarification? Should the file move forward or hold?

Once those states are clear, the bookkeeping team spends less time explaining the same file in different words. Leadership can also see whether delay is concentrated in missing inputs, reviewer load, or unresolved exceptions. That visibility makes later automation safer because the system is no longer guessing what the file state means.

Review breaks when intake ambiguity survives too long.

Reviewers frequently inherit the cost of weak intake design because ambiguity compounds by the time the file reaches them. A document may have arrived late, or in the wrong channel, or without enough context to confirm that it meets the requirement. The preparer may have worked around the gap temporarily. Notes may exist, but not in a standard format. When review begins, the reviewer has to decide whether the issue is substantive, procedural, or merely incomplete. That is not pure accounting work. It is workflow cleanup embedded inside review.

AICPA/CIMA quality-management guidance supports documented procedures, responsibilities, and monitoring.[3] In operator language, that means the bookkeeping workflow should not ask review to rediscover the intake state every time. The file should explain what was received, what remains open, and whether the missing support is routine or material. If that context is absent, the reviewer becomes the final intake diagnostician, which is usually the most expensive place for that labor to happen.

This is why document chaos can make a review queue feel much worse than the raw file count suggests. The queue is not merely processing volume. It is processing uncertainty. Reducing uncertainty upstream is often more valuable than adding pressure downstream.

It also explains why some firms feel that every review step takes longer than expected even when preparers are moving steadily. The reviewer is not only evaluating bookkeeping work. The reviewer is checking whether the supporting evidence and intake history are coherent enough to trust. If that coherence has to be rebuilt manually on each file, the review layer becomes a cleanup function instead of a control function.

What stronger review entry looks like

- a visible record of which required items were received and when

- a short unresolved-items summary attached to the file

- clear distinction between routine missing items and true exceptions

- a review-ready rule that blocks premature handoff

These are modest controls, but they reduce the amount of expensive context rebuilding that review would otherwise absorb.

Document chasing is a workflow signal, not just an annoyance.

Repeated document chasing is often treated as inevitable in client service. Some chasing is unavoidable. The more useful operational question is whether the firm can tell why the chase is happening. Is the original request unclear? Is the required-document list too vague? Did the item arrive through a channel the team does not monitor consistently? Is the client late, or is the workflow simply unable to see what has already arrived?

Industry accounting operations coverage commonly identifies delayed response loops and information chasing as recurring friction.[5][6] Under a process lens, those loops are not just communication burdens. They are evidence that the intake state, ownership model, or follow-up pattern lacks enough structure. If the same item is requested twice in one cycle, the workflow should ask what state failed, not merely who forgot.

This is where even simple measurements become useful. First-pass completeness, number of follow-up touches per file, open-item age, and non-approved-channel receipt rates can all help a firm understand whether document chaos is primarily a client responsiveness problem or a workflow design problem. Without that visibility, the team defaults to frustration instead of diagnosis.

When the same document needs to be chased twice, the workflow should assume it has a visibility problem until proven otherwise.

Ownership clarity matters as much as the checklist.

Checklists help, but they do not solve document chaos alone. A checklist without ownership still leaves the team asking who is responsible for moving the file from one state to the next. AICPA/CIMA guidance around quality management reinforces the importance of documented responsibilities and monitoring.[3] That principle applies directly to bookkeeping intake. Someone should own the state transition, someone should own follow-up, and someone should own escalation when the workflow cannot progress.

Without that clarity, documents may technically be missing but functionally unowned. Each team member assumes someone else is handling the follow-up, or assumes the system will surface the gap automatically, or assumes the client will send the item eventually. The file then sits in a kind of operational fog. Ownership rules bring that fog down to a visible next step.

These are bookkeeping workflow questions before they are software questions.

Once ownership is explicit, the team can also tell whether the workflow is failing because no one acted or because the system never made it clear who should act. That distinction matters. It changes the fix from generic accountability talk to concrete process repair.

In practice, firms often need to restate the exact ownership questions directly. Who confirms first-pass completeness? Who sends the routine follow-up? At what point does a delayed item escalate to a manager or controller? Who decides whether prep can continue with a temporary placeholder versus whether the file must hold? Writing those answers down is often more useful than adding another communications tool.

Blocked work should be separated from active work.

Document chaos becomes much harder to manage when blocked files remain mixed into the same visible queue as active production work. A bookkeeping file may appear to be in progress even though the next real step depends on a missing statement, an unanswered client question, or clarification of a contradictory attachment. If leadership cannot tell which files are truly workable and which are simply waiting, capacity planning becomes distorted.

That distortion matters because APQC-style process management depends on clear state visibility and reduced variation.[2] AICPA/CIMA quality-management concepts around monitoring and responsibilities support the same conservative interpretation.[3] A file waiting on client input is not the same as a file ready for transaction processing. A file waiting on internal clarification is not the same as a file ready for review. Once those states are blended together, the team starts solving the wrong problem.

Separating blocked from active work helps a firm answer more useful questions. Is the team genuinely short on processing capacity? Or is a large share of the queue stalled in the intake layer? Are reviewers overloaded with volume? Or are they absorbing files that should still be waiting upstream? Those distinctions are what turn complaint into diagnosis.

Useful queue distinctions for bookkeeping intake

- received but incomplete

- waiting on client response

- internally unresolved

- ready for bookkeeping work

- ready for review

- escalated exception

Those states are simple, but they help the system show whether the work is really moving or merely accumulating.

Technology helps most after the intake rules are already clear.

Document chaos is one of the easiest places to overestimate what new software or AI can fix by itself. If the workflow does not clearly define required items, approved channels, status transitions, and ownership, then a new tool will often preserve the same ambiguity in a cleaner interface. The firm may have more automation and still lack a trustworthy intake state.

That is why technology should usually come after the workflow becomes legible. Once the rules are clearer, software and AI can help draft follow-up, summarize missing items, route routine states, or surface aging blockers. Those are helpful uses because they operate inside a process the team already understands. Without that structure, the tool simply produces more activity around the same uncertainty.

This is also where an AI layer can become practical without becoming reckless. AI can assist with repeated coordination work around intake, but it should not decide that support is substantively sufficient when the rules are unclear or the evidence is contradictory. The distinction between workflow support and judgment remains important here.

Follow-up quality matters as much as follow-up frequency.

Many bookkeeping teams respond to document chaos by increasing the number of reminders they send. More reminders can help in some situations, but they are not the same as better follow-up. If the request language is vague, if the client cannot tell what satisfies it, or if the workflow does not show whether the item was partly received already, then additional touches may simply create more noise.

Industry coverage of bookkeeping and accounting operations often returns to the drag created by repeated document chasing and communication loops.[5][6] A process lens suggests that this is not only a volume problem. It is also a request-design problem. Better follow-up is more specific, more state-aware, and easier to act on. It tells the client what is missing, why it matters to the next step, and where it should go. That kind of precision reduces unnecessary back-and-forth even when the client is still late.

This is one place where AI can eventually help, but only after the bookkeeping workflow has already defined the required item, the approved channel, and the escalation path. The model can help draft a clearer message. It cannot invent the underlying intake rule responsibly if the firm has never defined it.

That distinction matters because many teams mistake faster drafting for better intake control. Faster drafting only helps when the workflow already knows what it is asking for and what state the file is actually in. Otherwise the firm simply sends more messages about a problem it has not fully defined.

Exception handling needs a visible path, not a hidden workaround.

Not every document problem is routine. Some files contain contradictory support, missing periods, unclear ownership, or evidence that does not fit the expected pattern. Those issues should not disappear into private side conversations or ad hoc notes. AICPA/CIMA quality-management concepts around documented procedures and remediation support the view that exceptions should follow an explicit path.[3]

That path does not need to be elaborate. It does need to be visible. The team should know what moves an item from standard follow-up into exception review, who owns that escalation, and what condition allows the file to re-enter the normal workflow. Without that path, exception handling quietly becomes another source of document chaos because nobody can tell whether the file is merely incomplete or substantively unusual.

Firms often underestimate how much calmer the workflow becomes once routine missing items and real exceptions are separated. The same queue becomes easier to read. Review becomes less cluttered. Staff stop treating every gap as equally mysterious. That is not a software miracle. It is better state design.

Secure handling and process discipline are linked.

Security is often treated as a separate issue from bookkeeping workflow design, but in practice the two are linked. IRS scam warnings and secure-handling concerns support the operational case for controlled channels and disciplined exchange practices.[4] A fragmented intake path is not only harder to govern operationally; it is also harder to supervise from a handling and compliance perspective. Every off-channel handoff weakens both visibility and control.

This does not mean a bookkeeping firm can reduce document chaos to a security policy. But it does mean that cleaner intake discipline creates a dual benefit. It helps the team know where the document is and helps the firm know whether it moved through the expected lane. That combination is especially useful in environments where multiple team members touch the file before review is complete.

Seen this way, the intake process is not merely clerical administration. It is part of the firm’s operating control environment.

What a cleaner bookkeeping intake workflow looks like.

A cleaner intake workflow is not necessarily more complex. In many cases it is simpler because it removes ambiguity. The required-document list is defined for recurring work. The authoritative intake path is clear. Off-channel items are normalized into that path instead of living permanently on the side. File states answer real workflow questions. The next owner is visible. Open-item age can be seen without private memory. Review does not start unless the stated gate is met or a named exception path has been chosen.

That kind of workflow does not eliminate late documents or client delay. It does change how much confusion those realities create inside the firm. Instead of every missing item becoming a small detective story, the workflow makes the missing state explicit and easier to act on. That is the real operational value.

It also changes how improvement work is prioritized. Once the intake states are reliable, leadership can see whether the next constraint is client responsiveness, internal capacity, review discipline, or exception handling. Without that clarity, every problem tends to get described as “document chaos,” even when the true blocker has shifted elsewhere in the process.

This is the point where later automation becomes more credible. A bookkeeping team that can already define what is missing, who owns the next step, and when an item becomes an exception is in a much better position to let technology assist with reminders, summaries, and routing. A team that cannot answer those questions yet is likely to get more motion without more trust.

Questions worth asking in a document-chaos review

- Can we tell, without searching multiple channels, whether the required record was received?

- Do our intake states mean the same thing to intake, prep, and review?

- How many follow-up touches are caused by unclear state rather than by true client delay?

- At what point does a missing item escalate, and who owns that escalation?

- How often does review reopen the file because the intake picture was incomplete?

- Which off-channel behaviors are tolerated, and how are they normalized back into the workflow?

If those questions are hard to answer, the bookkeeping team is likely carrying more intake ambiguity than it realizes.

The bottom line

Client document chaos is not a minor admin nuisance sitting beside bookkeeping. It is one of the main ways bookkeeping workflows lose trust in their own input state. IRS guidance supports the principle of complete document gathering before downstream action.[1] APQC supports standardization and reduced variation.[2] AICPA/CIMA quality-management guidance supports documented procedures, responsibilities, monitoring, and remediation.[3] IRS security-oriented guidance supports controlled exchange practices.[4] Industry workflow coverage supports treating document chasing as recurring operational friction rather than as a one-off complaint.[5][6]

The practical conclusion is that the fix begins with clearer intake states, more reliable ownership, a smaller number of authoritative channels, and better downstream visibility. Once those are in place, technology and AI can help around the repetitive coordination layer. Until then, the firm is likely automating confusion.

That conclusion is valuable precisely because it is modest. It does not require a bookkeeping firm to solve every operational issue at once. It asks the firm to make the intake layer more trustworthy so that the rest of the workflow stops paying for the same ambiguity repeatedly. In many cases, that is the highest-leverage improvement available because it reduces rework before rework has a chance to spread into prep, review, and client communication.

Firms that handle this well are not necessarily the firms with the most software. They are the firms whose workflow can answer basic intake questions quickly and consistently: what is missing, what was received, who owns the next move, and whether the file is truly ready to advance. That is the operating standard that makes later automation and AI assistance worth installing.

If you want to stop rebuilding the same intake chaos every cycle

Intelligence Solved helps bookkeeping teams clarify intake states, tighten the source of truth, define ownership, and add automation only after the workflow is clear enough to trust.

Sources

- IRS, “Get ready to file in 2025: IRS highlights what taxpayers should know before filing in 2025,” irs.gov.

- APQC, process and finance benchmarking resources, apqc.org.

- AICPA/CIMA, quality management standards resources, aicpa-cima.com.

- IRS, Dirty Dozen tax scams overview, irs.gov/newsroom/dirty-dozen.

- Accounting Today, accounting operations and workflow coverage, accountingtoday.com.

- Thomson Reuters Institute, tax and accounting operations coverage, thomsonreuters.com.