The most frustrating close is not the one that is obviously broken.

It is the one that looks mostly done.

The bank accounts are mostly reconciled. The recurring transactions are mostly posted. Payroll is mostly handled. The client has answered most of the questions. The checklist has more checked boxes than open boxes.

And yet the file still is not ready.

There is a bank-feed exception that needs context. A payroll report is missing. A loan balance needs support. A reviewer left a note that no one owns yet. The reporting package needs an explanation for a variance. A client answered one question but created two more.

This is where month-end close drags for many bookkeeping and CAS teams.

The team does not have a pure task problem. It has a readiness problem.

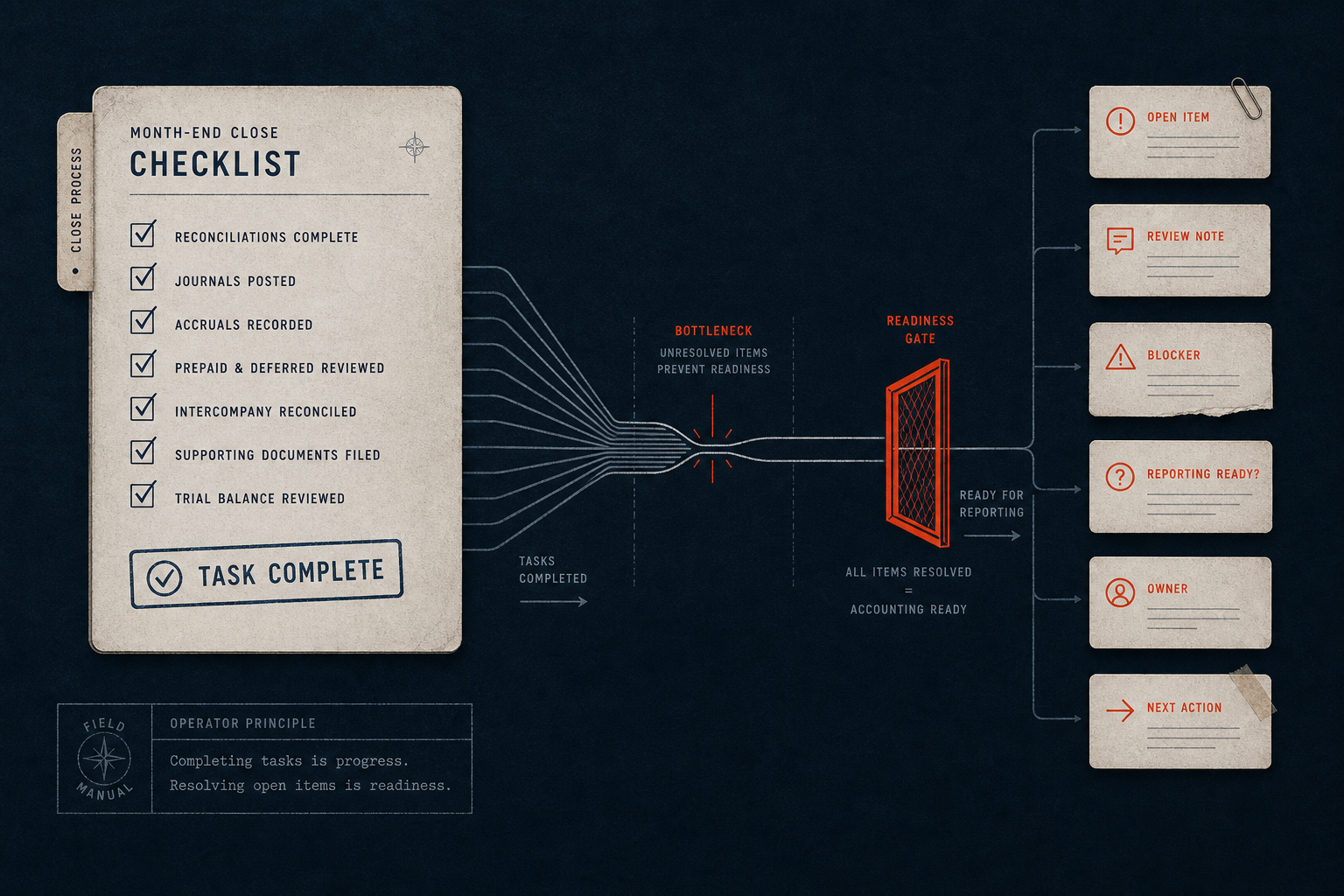

Task complete is not the same as accounting ready

A task can be complete in the task system and still not be ready for accounting review.

That distinction is easy to miss.

Task completion means an activity was checked off. Someone touched the reconciliation. Someone requested the statement. Someone reviewed the uncategorized transactions. Someone sent the client questions.

Accounting readiness means the work can move forward without someone reconstructing the context.

That requires more than a checked box. It requires:

- evidence

- unresolved question

- owner

- status

- blocker

- review note

- next accounting action

If those pieces are not clear, the work may be active, but it is not ready.

This is why the final part of close can feel heavier than the first part. The obvious tasks are done. What remains is not always a task list. It is a set of unresolved context fragments.

Common close drag points

Public month-end close content commonly names source completeness, reconciliations, payroll and loan support, uncategorized transactions, client questions, review, variance explanations, and sign-off. Those categories are real. They show up because firms repeatedly hit the same close friction.

The operational problem is what happens inside those categories.

A client answer may arrive without enough detail. A payroll file may be uploaded, but for the wrong period. A bank-feed exception may need judgment from someone who is not currently in the file. A review note may say "confirm treatment" without a clear owner or source. A reporting explanation may depend on a decision made three weeks ago in an email thread.

Nothing about that is solved by checking "client questions sent" or "review started."

The question is whether the team can see the real status:

- What is still open?

- Why is it open?

- Who owns the next move?

- What evidence exists?

- What decision or answer is needed?

- What happens if it does not arrive before close?

When those answers are scattered, close slows down.

Checklists are necessary but insufficient

Close checklists matter. A firm without a checklist usually has a sequencing problem on top of every other problem.

But a checklist can create false comfort if it tracks activity instead of readiness.

"Reconciliation reviewed" is not enough if the exception is still unresolved.

"Client questions sent" is not enough if no one owns the follow-up.

"Payroll support requested" is not enough if the file received does not match the period being closed.

The checklist should not disappear. It should become more honest.

A useful close workflow distinguishes between:

- not started

- in progress

- waiting on client

- waiting on internal review

- evidence received but not accepted

- blocked by accounting question

- ready for review

- ready for reporting

That kind of status makes the close easier to manage because it exposes the real state of the work.

More staff does not fix unclear context

When close is dragging, the natural answer is often: "We need more staff."

Sometimes that is true. Capacity matters.

But more staff does not automatically fix a workflow where every unresolved item has to be rediscovered during handoff or review.

In some cases, more people can increase the number of handoff surfaces. The preparer knows one piece. The reviewer knows another. The client manager has the email context. The owner remembers the prior-month exception. The task system says one thing while the accounting file shows another.

Now the team has more hands, but not more shared context.

That is why staffing and workflow design should not be treated as opposites. A better workflow makes current staff more coherent and makes future staff easier to onboard into the process.

The close does not only need people doing work. It needs the work to carry its status, evidence, blocker, owner, and next action.

What a close workflow needs

A stronger month-end close workflow makes unresolved context visible.

For a small bookkeeping or CAS team, that usually means defining:

- close owner and item owner

- evidence status

- review readiness status

- blocker categories

- next accounting action

- escalation timing

- carryforward rules

- reporting narrative handoff

The goal is not to make a giant process manual. The goal is to remove ambiguity from the recurring close points that create drag.

If a client answer is missing, the workflow should show who owns the follow-up and what the answer blocks.

If evidence is received but incomplete, the workflow should show that it is not accepted yet.

If a review note needs judgment, the workflow should show who needs to decide and what information they need.

If an item cannot be resolved this month, the workflow should show how it carries forward instead of vanishing into memory.

This is the difference between closing tasks and closing context.

Where AI-assisted workflow design can help

AI-assisted workflow support can be useful when the firm has already defined the workflow objects.

It can help summarize close status. It can draft follow-up language for missing items. It can help route review notes. It can prompt the team when an item lacks evidence, owner, or next action. It can help turn messy notes into a cleaner close-readiness view.

But AI should not approve reconciliations. It should not choose accounting treatment. It should not override reviewer judgment. It should not make compliance decisions.

The safer and more useful role is support around context handling.

That is the services-first position for Intelligence Solved. Diagnose the recurring close bottleneck. Define the operating context. Install the workflow around the team's actual close pattern. Keep human judgment and review in the right places.

This is not a pitch for another dashboard.

It is a way to stop rebuilding the same close context every month.

The better first step

If month-end close keeps dragging, do not start with a broad transformation project.

Start with one recurring close bottleneck.

Which item shows up every month? Which handoff breaks down? Which review note creates rework? Which client answer stalls reporting? Which open item keeps forcing the manager to rebuild status from memory?

That is the best diagnostic starting point.

Book a fit call if month-end close keeps stalling on the same unresolved items, or send Intelligence Solved the bottleneck your team keeps rebuilding every month.