The most dangerous question in accounting right now is not “What can AI do?” It is “What can we stop thinking about?” That is where firms get sloppy. Automation can remove touches, package context, and speed up repetitive work. It should not quietly erase responsibility.

Some accounting tasks should never be fully automated. Not because software has no value, but because the task itself requires skepticism, context, defensible judgment, or human ownership when the cost of being wrong is material.

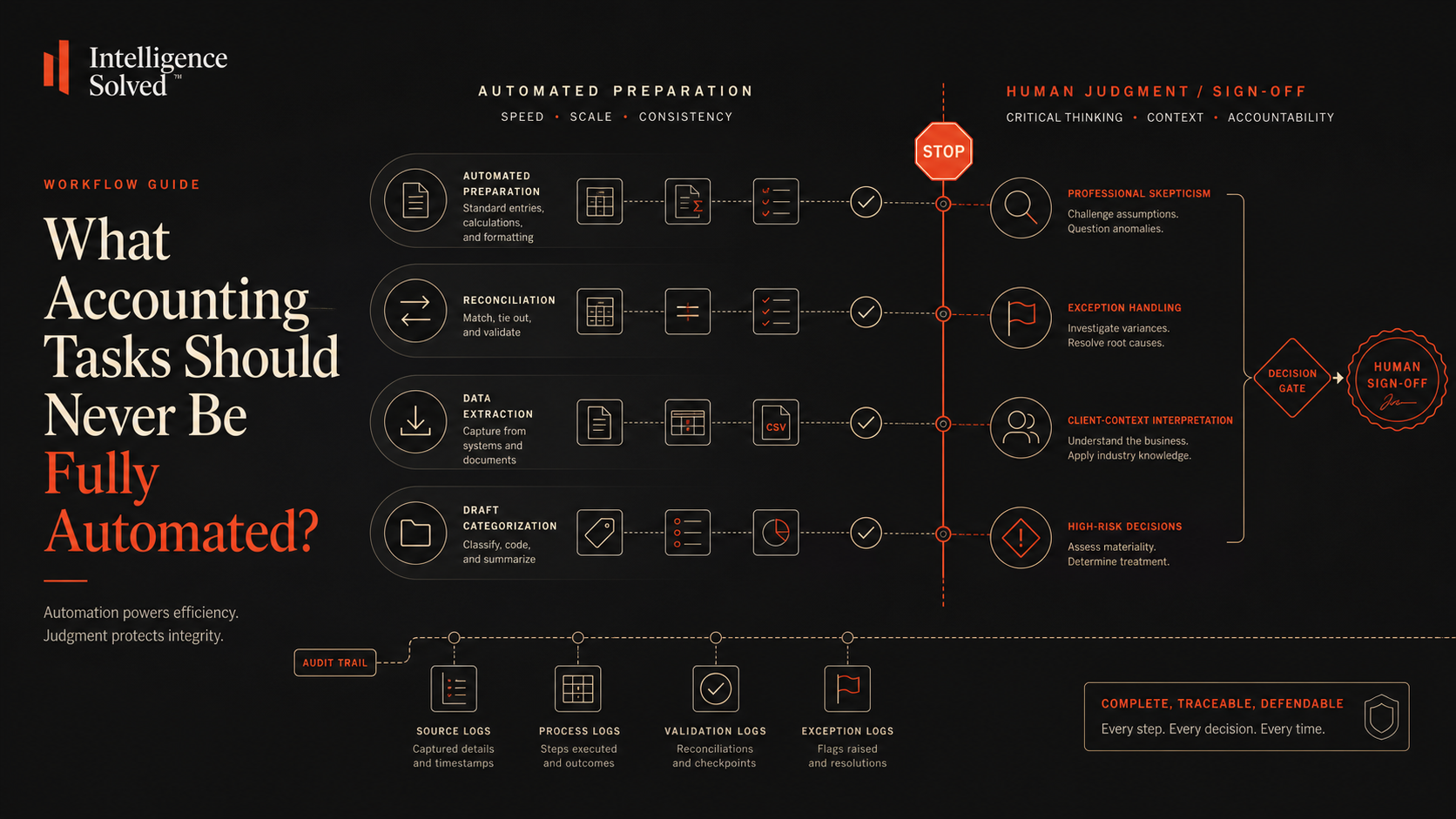

The clean rule

Automate repetition. Keep humans on judgment. That single boundary will protect a firm better than most AI hype ever will. The mistake happens when leaders confuse “the system produced an answer” with “the work no longer needs accountable review.” Those are not the same thing.

Tasks that should never be fully automated

1) Final review and sign-off

A system can draft, summarize, classify, route, and package. That does not mean it should own the final answer. Someone still has to decide whether the work makes sense, whether the support is enough, whether the treatment is defensible, and whether they would stand behind it if questioned later.

Final review is not just a formatting pass. It is where professional accountability becomes real.

2) Professional skepticism

This is one of the biggest boundaries. AI can produce a wrong answer with the same confidence and polish as a correct one. That means a human still has to be willing to say, “This looks clean, but I do not trust it yet.” Automation does not replace that instinct. If anything, it makes that instinct more important.

3) Exception handling

Automation loves stable patterns. Accounting pain usually lives in broken patterns. New vendors, mixed-use expenses, odd transfers, missing support, prior-period messes, one-off owner behavior, and unusual timing questions are exactly where a human still earns their keep.

If the workflow tries to flatten exceptions into the same lane as routine work, the quality problem does not disappear. It just moves downstream.

4) Client-context interpretation

The ledger line is not always the whole story. Sometimes the right answer depends on client intent, business behavior, missing narrative, supporting explanation, or repeated issues that reveal a deeper control problem. A system can surface the question. A human still has to interpret what the answer means.

5) High-risk accounting decisions

If the cost of being wrong is expensive, embarrassing, regulatory, or trust-damaging, a human should own the decision. That is the cleanest rule. Automation can prepare the packet. It should not silently inherit the accountability.

What is still fair game for automation

This boundary does not mean firms should automate nothing. It means they should automate the right layer. Repetitive preparation work, first-pass packaging, missing-item follow-up, extraction, matching, standard formatting, and bounded summaries are all much safer candidates. The rule is not “avoid automation.” It is “aim it at the right part of the workflow.”

The best AI installs reduce low-value touches before the judgment layer rather than trying to eliminate the judgment layer entirely.

Why this matters operationally

When firms lose this boundary, one of two bad things usually happens. Either senior people stop trusting the workflow because they know too much is being handed off too casually, or junior people start relying on polished outputs they should still be interrogating. In both cases, the firm thinks it improved speed while quietly weakening trust.

A better workflow makes the human role clearer, not blurrier. The system should do the boring parts better. The reviewer should do the consequential parts more intentionally.

A practical test for your firm

Take any task you are considering for automation and ask three questions. First: if this is wrong, who pays for it? Second: what context would a qualified human want before approving it? Third: could a system miss something important while still sounding confident? If the answers point toward risk, ambiguity, or accountability, the task does not belong in a fully automated lane.

Closing thought

You can automate preparation. You should not automate responsibility. Firms that protect that line will get more from AI because they will use it where it actually strengthens the workflow instead of where it quietly weakens judgment.